«Данное сообщение (материал) создано и (или) распространено иностранным средством массовой информации, выполняющим функции иностранного агента, и (или) российским юридическим лицом, выполняющим функции иностранного агента»

Topic: Oil and Gas, and Trade Blog Brand: Energy World Region: Americas, Eurasia, and Middle East Tags: China, Energy Security, Iran War, Liquefied Natural Gas (LNG), North America, Russia, Siberia 2 Pipeline, and United States How China Became Asia’s Energy Middleman April 15, 2026 By: Fyodor Dmitrenko

Topic: Oil and Gas, and Trade Blog Brand: Energy World Region: Americas, Eurasia, and Middle East Tags: China, Energy Security, Iran War, Liquefied Natural Gas (LNG), North America, Russia, Siberia 2 Pipeline, and United States How China Became Asia’s Energy Middleman April 15, 2026 By: Fyodor Dmitrenko

Share

The Iran War revealed what years of pipeline deals and LNG contracts quietly built: a Chinese stranglehold on Asia’s gas supply.

When Reuters reported that Chinese companies had resold a record 19 LNG cargoes in the first quarter of 2026 alone—10 to South Korea, five to Thailand, and the rest split among Japan, India, and the Philippines—the story was framed as shrewd trading. And it was. Russian pipeline gas costs Beijing around $250 per thousand cubic meters. Asian spot prices had blown past $830. The markup was obscene. But the story behind the story is far bigger than one quarter’s arbitrage profits.

What the Iran War has done is tear the wrapping off a structural shift a decade in the making. China is not merely reselling surplus gas. It is building something no country has attempted before: a three-tier supply architecture that makes it the swing supplier for the entire Asia-Pacific. Buy cheap overland, contract massive liquefied natural gas (LNG) volumes worldwide, release the surplus to neighbors at whatever price the market—or the crisis—will bear.

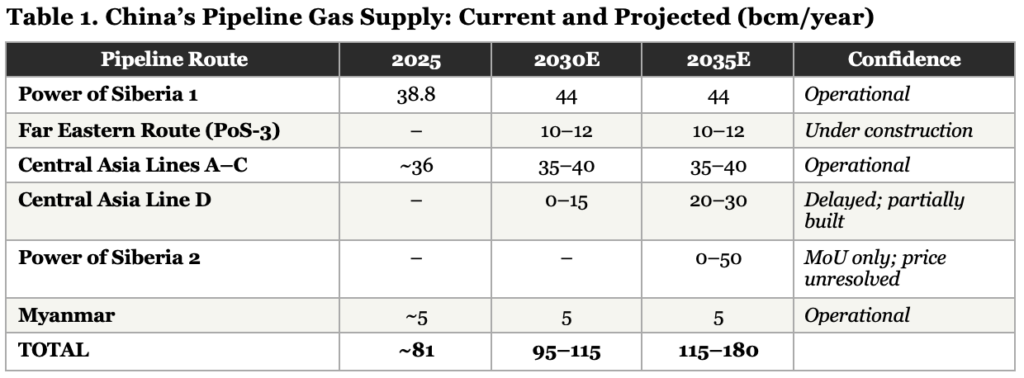

China’s Expanding Pipeline Network and Eurasian Gas Supply Routes

In 2025, Gazprom pushed 38.8 billion cubic meters (bcm) through Power of Siberia 1 (PoS-1)—more than its contractual maximum, more than all pipeline exports to Europe, including Turkey combined. Five years ago, that would have been front-page news. Today, it barely registers because the pipeline map keeps expanding.

The Far Eastern Route—sometimes called Power of Siberia 3—is scheduled to begin deliveries in 2027. Initial flows will be small, around two bcm, but the design target is 10-12 bcm per year, fed from Sakhalin’s offshore fields. In September 2025, Gazprom and China National Petroleum Corporation (CNPC) agreed to raise the combined throughput of PoS-1 and the Far Eastern Route to 56 bcm, up from the previously contracted 48 bcm. These are not aspirational numbers. The steel is in the ground.

On the Central Asian side, Turkmenistan already delivers about 40 bcm a year through three parallel lines of the Central Asia-China pipeline, making it China’s single largest pipeline supplier. CNPC began Phase four commercial development of the Galkynysh field—the world’s second-largest gas deposit—in early 2026. And then there is Line D: a fourth pipeline through Tajikistan and Kyrgyzstan that would add another 30 bcm. President Xi Jinping has personally pushed Central Asian leaders to speed it up. Construction has been plagued by delays, but one critical Tajik tunnel is complete, and the political will looks stronger than at any point in the project’s tortured history.

Power of Siberia 2 (PoS-2) is the project that could change the picture entirely—if it happens. The proposed 50 bcm pipeline from Yamal through Mongolia would redirect the very molecules that once heated German homes toward Chinese factories. A legally binding memorandum was signed in September 2025. More telling, China’s 15th Five-Year Plan, approved by the National People’s Congress in March 2026, included the pipeline—but only in the language of “advancing preparatory work.” That is a political signal, not a commercial commitment. Price remains the central sticking point: Beijing has pushed for terms closer to Russia’s subsidized domestic rate, while Gazprom needs something higher to keep the project above water. The Iran War may give it a push—overland supply insurance looks more valuable when tankers cannot get through—but even under optimistic assumptions, gas will not flow before the early 2030s.

Sources: Gazprom, CNPC, Columbia CGEP, Caspian News, Global Energy Monitor. Author’s assessment.

Sources: Gazprom, CNPC, Columbia CGEP, Caspian News, Global Energy Monitor. Author’s assessment.

China’s Gas Supply-Demand Imbalance and LNG Resale

Here is where the arithmetic gets interesting. China’s domestic gas production hit 262 bcm in 2025, climbing by 13-16 bcm every year for six straight years. Sichuan’s shale gas fields are ramping fast. The 15th Five-Year Plan is expected to push unconventional output even harder. Kpler projects 278 bcm in 2026, with 300–320 bcm within reach by 2030.

Then there is the nuclear build-out, which matters more than most energy analysts give it credit for. China has 39 reactors under construction, over 35 gigawatts (GW) worth of installed capacity, and the State Council has been approving ten or more new units every year since 2022. Each gigawatt of nuclear takes roughly 1.5–2 bcm of gas out of the power generation mix. That is 50-70 bcm of gas demand that simply disappears as those reactors come online through 2032. Wind and solar, meanwhile, reached 1,760 GW of installed capacity by the end of 2025. A 34 percent jump in one year.

Now set all that against the contract book. Chinese buyers hold over 65 million tonnes per annum in long-term LNG contracts, a figure that the Center for Strategic & International Studies (CSIS) expects to keep climbing. Many of these deals, especially those with American suppliers, carry destination flexibility: the buyer can redirect cargoes wherever it likes. By 2030, contracted LNG volumes may reach 130-150 bcm. Actual domestic LNG consumption, squeezed from both sides by rising pipeline imports and domestic production, may only need 100–120 bcm.

The gap between what China has contracted and what it actually burns is the resale surplus. Right now, the gap is narrow—maybe 5-15 bcm. By 2030, it could widen to 15-50 bcm. By 2035, if even a partial version of Power of Siberia 2 comes through, the surplus could hit 30-70 bcm. Those are not rounding errors. Seventy bcm exceeds Japan’s entire annual LNG import volume.

Strait of Hormuz Disruption and China’s Energy Security Advantage

Before February 28, this was a theory. After February 28, it became policy.

When the United States and Israel struck Iran and the Islamic Revolutionary Guard Corps (IRGC) choked the Strait of Hormuz, Asia’s energy importers had good reason to panic. Japan gets 93 percent of its oil through the Strait of Hormuz. Qatar’s Ras Laffan LNG complex, the world’s largest, declared force majeure after a drone attack. The Philippines hadless than 10 days of diesel left and declared an energy emergency. Over 40 percent of gas stations in Laos shut down.

China took a hit, too. It sources roughly 40 percent of its crude and 30 percent of its LNG through Hormuz. But it had something no one else in Asia did: a pipeline buffer that never touches saltwater. Russian and Central Asian gas kept flowing. Domestic shale production did not miss a beat. Beijing halted gasoline and diesel exports in March, tightening regional supply even further, and then selectively released fuel shipments to the Philippines and Vietnam—two countries that found themselves depending on Chinese goodwill for basic energy access.

The LNG resales were the most visible part. In March alone, China flipped eight to 10 cargoes, a monthly record, to buyers who had nowhere else to turn. Some of those cargoes came from Russian projects. Japan, which sanctions Russian energy, bought it anyway. The alternative was blackouts.

China’s Role in Global LNG Markets: Not a Competitor, but a Market Shaper

The emerging narrative—China as America’s LNG rival—confuses the symptom with the condition. The United Stateswill bring roughly 260-270 bcm of LNG export capacity online by 2030, over 30 percent of global supply. China does not liquefy a single cubic meter for export. As a straight production contest, there is no contest.

But China is not in that contest. It is running three different games at once.

The first is price arbitrage compression. Every cargo China dumps onto the Asian spot market adds liquidity and pushes prices down, eroding the premium American producers depend on. US Gulf Coast LNG breaks even at roughly $7-9 per million British thermal units (MMBtu) delivered to Asia. When Chinese resales pile up, the spot price drifts toward $6 or lower. Projects still waiting for a final investment decision start to look uneconomic, and capital hesitates.

The second is structural demand destruction. Every bcm of Russian or Turkmen pipeline gas that enters China’s grid is a bcm of LNG that the country does not need from anyone else. If Power of Siberia 2 delivers even 30 of its 50 bcm design capacity, that alone would wipe out an amount of Chinese LNG demand equal to the entire output of a major US export terminal. Add the nuclear and renewable build-outs, and China’s hunger for seaborne gas starts to look increasingly bound—at exactly the moment when global LNG supply is about to surge.

The International Energy Agency’s (IEA) latest forecast puts the LNG surplus at about 65 bcm by 2030 in the base case. The IEA World Energy Outlook 2024 estimated surplus liquefaction capacity at 130 bcm under the Stated Policies Scenario—about 15 percent of global capacity with nothing to do. Qatar, with breakeven costs near $3.80-3.90 MMBtu, can ride that out. Most everyone else cannot.

The third game is crisis-period leverage, and it is the one that should worry policymakers in Tokyo, Seoul, Manila, and New Delhi the most. When the Strait of Hormuz closed, China was the only major Asian economy with surplus gas to offer. That was not generosity. It was leverage. Beijing sent diesel tankers to the Philippines only after Manila’s energy emergency became acute. The message to every energy-dependent neighbor was not subtle: your supply security runs through us now.

China’s Three-Tier Energy Strategy

Step back, and the logic of the system becomes visible. Tier one is energy security in its purest form: overland pipeline gas from Russia and Central Asia, immune to naval blockades and chokepoint politics. Committed capacity today sits at about 95 bcm. It could reach 130-180 bcm by 2035, depending on what happens with Line D and PoS-2.

Tier two is the flexible LNG portfolio. Chinese state companies and private firms have been signing contracts at a pace that will outstrip domestic needs—deals with US, Qatari, and Australian suppliers, many with built-in destination flexibility. Every surplus cargo becomes a tradeable asset. China’s growing fleet of LNG carriers cuts dependence on foreign shipping. Regasification capacity is set to double, reaching 250 bcm by 2027.

Tier three is the domestic production buffer. Output went from 209 bcm in 2020 to 263 bcm in 2025—shale gas in Sichuan, tight gas in the Ordos Basin, coalbed methane in Shanxi. Unconventional sources now account for 47 percent of total production. Import dependence has held steady at 40-41 percent even as total consumption keeps climbing.

Taken together, these three tiers produce something without precedent in global energy markets: a country that is simultaneously the world’s largest gas importer and a growing gas re-exporter. Not because it has gas to spare, strictly speaking, but because it has arranged things so that its cheapest sources—pipelines, domestic wells—cover base demand, and its most expensive source, LNG, can be dialed up or sold off depending on the season, the price, or the geopolitical weather.

The comparison that keeps coming up in policy discussions is rare earth minerals. China cornered upstream supply, made itself the indispensable middleman, and built leverage that proved very hard to undo. The gas version of that playbook is taking shape right now.

What Washington and Tokyo Should Worry About

For American LNG producers, the timing is brutal. The United States is about to bring online the largest wave of liquefaction capacity in history—roughly 100 bcm of new export capacity by 2028, with more to follow. Those projects were greenlighted on the assumption that Asian demand, Chinese demand above all, would keep growing. Maybe it will. But every pipeline bcm from Russia or Turkmenistan that reaches China is a bcm of LNG demand that disappears from the addressable market. And if Chinese buyers keep redirecting their US-origin cargoes to third countries—as they have been doing to dodge tariffs—American molecules end up competing against themselves in Southeast and South Asian markets.

For Japan, the problem cuts deeper. The Iran war has exposed a dependency that Tokyo has understood for decades but never fixed. Ninety-three percent of Japan’s oil and a large share of its LNG pass through the Strait of Hormuz. When it closed, Japan found itself buying Chinese-resold cargoes that probably contained Russian gas—gas that Tokyo’s own sanctions were meant to keep out. The cognitive dissonance was manageable. The strategic exposure is not.

South Korea, India, the Philippines, and Thailand face variations of the same dilemma. None has overland pipelines to major gas producers. All depend on sea lanes that run through at least one chokepoint. China alone among the major Asian importers has built a land-based alternative. And it is using that alternative not just for its own energy security but as a tool of commercial and political influence across the region.

None of this happened by accident. Beijing spent 15 years and hundreds of billions of dollars building this position: the pipelines, the LNG terminals, the long-term contracts, the shale gas campaigns, the nuclear energy reactors. The Iran War did not create China’s energy leverage over Asia. It revealed it. For the countries now scrambling for fuel, the revelation came too late to matter.

About the Author: Fyodor Dmitrenko

Fyodor Dmitrenko is a geopolitical analyst and researcher specializing in sustainable development, energy policy, and governance on the Eurasian continent. He is affiliated with Sciences Po Paris, where he conducts research under the supervision of Professor Tatiana Mitrova. He has contributed articles on developments in energy markets and international trade flows at Reuters News Agency’s CIS office and for emerging think tanks such as India’s TheGeostrata and the Paris section of the French-MFA-affiliated Andalus Committee, which deals with EU-global south relations. He has also engaged with leaders in the sustainable development field at the Guiyang Ecological forum as a Sciences Po delegate to the Tsinghua Global Youth Dialogue, and interviewed policy makers such as former Brazilian central bank head Gustavo Franco and former Swiss President Simonetta Sommaruga as the Sciences Po delegate to the Warwick Economic Summit.

The post How China Became Asia’s Energy Middleman appeared first on The National Interest.

Источник: nationalinterest.org